By Nick Fisher, Portfolio Manager

As the year unfolds, evidence is mounting that the economy is slowing, with multiple factors at play. The Federal Reserve reversed course quite suddenly at the end of December from raising rates to a more neutral, and even accommodative, stance. Some have begun to question whether we may see recession in 2020. With this bull market approaching the longest in history, valuations are high as we have discussed many times. But now we see the near possibility of economic contraction; the Dow Jones Industrial Average and S&P 500 have near zero return over the last 18 months. We will proceed with maximum caution, but, as the market plays out, we are seeing more opportunities reveal themselves.

Morgan Stanley’s economic cycle indicator below shows the risk of a downturn is at its greatest point since this recovery began.

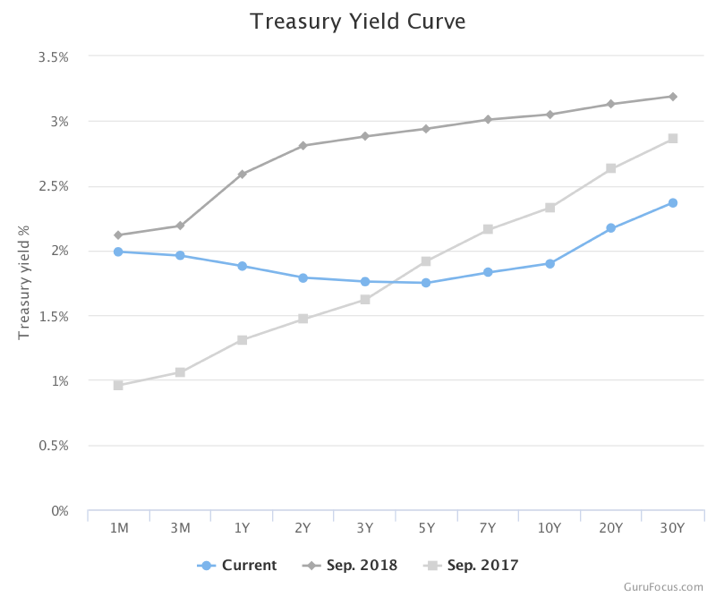

Yield Curve

The yield curve is the prime culprit. Treasury bond investors have been willing to tie up their money for 10 years at a lower rate, currently 1.55%, compared to the 3 month rate of 2.06%. It doesn’t make much sense that investors are willing to do that unless in the short-term they expect recession. The inverted yield curve as they call it, has been a great indicator of recession.

Professor Campbell Harvey of Duke University is probably the nations’ foremost expert on the inverted yield curve and his doctoral dissertation (reviewed by 3 Nobel Prize winners) has accurately predicted every recession in the past 40 years. Harvey considers the models accuracy definitive if the indicator remains for an entire quarter. “Unconditionally, it means slower economic growth is coming.” We’ll know “definitively” in time.

The biggest positive for the economy has been the persistence of negative rates in Europe. Ken Fisher was quoted on Bloomberg saying that the differential in rates between Europe and US has been a boon for money flows. Indeed, banks in the US are borrowing with near 0% rates in Europe and lending money in the US at a higher rate.

The stimulative effect, or at least the offset to tightening monetary policy, has been significant. The Fed’s measure of commercial and industrial lending corroborates this over the last year. Importantly, the growth in lending has slowed considerably in the last several months.

If we see a recession here in the United States, it appears that it should be relatively mild compared to recent memory of the global financial crises. We just haven’t seen significant excesses (other than in the corporate bond market). Real GDP growth may be muted, but will continue to grow over the next few years. Asset prices here in the United States may be a different story: the narrative around technology stocks and some of the other high flying stocks are beginning to show some chinks in their armor. We believe this will inevitably lead to a migration into cheaper stocks which have persistently underperformed for the last many years and likely will reverse course in a downturn of more expensive stocks. This shift will benefit our portfolios as we have been positioning accounts for this sea change.

Portfolio Updates

Early in 2018 we bought commodities in order to protect our cash and fixed income investments from inflation. But with the slow global economy and inverted yield curve, the threat of inflation has subsided, and we have sold the last bit of our broad-based commodities exposure. Instead we have added the Cambria Tail Risk ETF to portfolios which is designed to steady your portfolio. It also adds bond market exposure and if history is a guide, it will protect our capital from a broad, persistent decline in the US stock market.

This added level of safety will allow us to continue to add exposure to stocks in areas that we find much cheaper than the broader market. An example:

Kraft Heinz (KHC): I challenge anyone to go to a BBQ and not find a Kraft Heinz product on the condiment table. Over the last two months I have yet to find one instance of Kraft Heinz not represented. Sure, Berkshire Hathaway admitted to paying too high of a price in the acquisition of Kraft and certainly Kraft is under some pressure in stores to better market and cleanup its product offerings. But, with their largest investor Warren Buffett looking after our investment, I’m quite confident that over the coming years they will pay down debt and get back to the roots of running the company (rather than looking for its next acquisition). In the meantime, the stock is paying a 5.5% dividend!

Conclusion

We will continue to be cautious as we manage your capital. We see opportunity today and ahead, but we will likely experience much more volatility in the next 18-24 months. As most of you know, our portfolios are positioned to weather this volatility. The biggest mistake investors make is projecting forward recent returns. The seeds for future returns are sown in times of uncertainty. We’ll buy when investors are most pessimistic.

We thank you for trusting us with your well-deserved and hard-earned funds.